If you regularly follow watch industry news, you've likely seen Morgan Stanley's report on the top 50 Swiss watch brands.

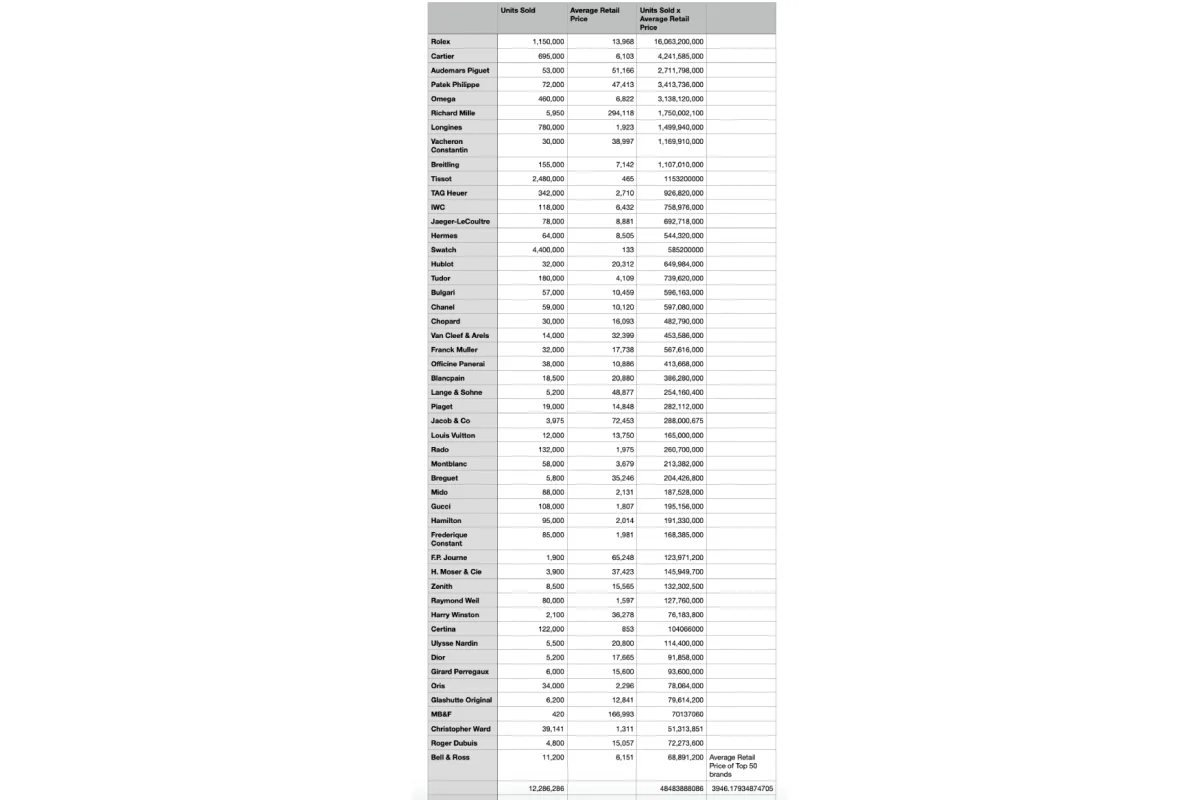

The main takeaway, if you missed it, is that Rolex continues to dominate the industry, generating revenue that surpasses the combined turnover of the next four leading brands. Omega dropped from third to fifth place in total turnover, with sales decreasing by 45,000 units in 2025 (from 505,000 units in 2024 to 460,000 in 2025).

Cartier holds the second spot, increasing both the number of watches sold and the average retail price. Audemars Piguet and Patek Philippe have improved their positions by raising the average sales price and sales volumes. Now that the major brands and price categories have been reviewed, what do these numbers mean for the average enthusiast?

For the "Average" Watch Buyer

In a study comparing the enthusiast car market with the watch market, I found that the average retail price of watches from the top 50 brands in 2024 was 3,595.98 Swiss francs (CHF). This price is optimal for many brands popular among enthusiasts, such as Tudor and Longines, especially for models with complications. In 2025, the average price rose to 3,946.18 CHF, an increase of 9.8%. The average sales price of Tudor increased from 3,259 CHF in 2024 to 4,109 CHF in 2025 (a 26% rise), while Longines' price remained almost unchanged at 1,922 CHF in 2024 and 1,923 CHF in 2025. Meanwhile, Tudor's sales volume grew from 160,000 to 180,000 units, whereas Longines' fell from 950,000 to 780,000 units.

These data points are intriguing for several reasons. Firstly, global inflation in 2025 was estimated at 4.2%, meaning the 9.8% increase in average price significantly exceeds inflation. Secondly, Tudor's 26% increase in average price compared to Longines' slight 0.05% increase (1 CHF) indicates market shifts beyond simple inflationary and economic policy effects.

Tudor's performance in 2025 indicates that, besides raising prices, the brand has successfully convinced buyers to move into a higher price segment, encouraging existing customers to consider more expensive models. It can also be suggested that many potential buyers, who were considering more premium brands, were "priced out," making Tudor the best option for disappointed buyers. If one can't buy a Submariner or a Seamaster becomes unaffordable, the Tudor Black Bay seems a logical choice.

While Longines impressed enthusiasts with the updated Spirit line in 2025, it did not translate into sales growth: volumes declined, and the average price remained unchanged (even the base Spirit model with only time display is priced above Longines' average price).

Transition to More Expensive Segments

Longines' performance reflects an overall trend within the Swatch Group: most of the group's brands showed declining results from 2024 to 2025. Many major Swatch Group brands are focusing on premium offerings (Omega, Blancpain, Breguet, and partially Longines), which seems to reduce interest among enthusiasts despite the brands' efforts. Despite the improvement in product quality, these brands' perception among the general public is not strong enough to attract casual buyers, and moving up the price ladder alienates some loyal fans, even if price increases are justified by inflation and quality improvements.

A case in point is the Longines Legend Diver, which used to sell for $2,500, and now the new models are priced at $3,850 on a bracelet. Although the new watches feature improved movements with increased power reserve, silicon components, and updated bracelets, the price increase of more than 50% is hard to justify, especially for less experienced collectors.

Omega and Jaeger-LeCoultre: Different Paths

Although I've mentioned them at the beginning, it's worth returning to Omega and Jaeger-LeCoultre. As I wrote in an article comparing the automobile and watch markets, these two brands lost some of their enthusiast audience - and notably active parts of it. Despite both brands always being positioned as premium (especially JLC), they offered good value for money. Aggressive price hikes in recent years have impacted Omega's results. Jaeger-LeCoultre, on the other hand, maintained stability with a slight decrease in sales in 2025 compared to 2024.

I believe that JLC's more premium positioning and its customer base accustomed to high prices contributed to the brand's stability, while Omega's performance declined. Brands are rarely ready to lower prices as it could damage their image. Omega should focus on increasing product value, particularly in aspects understandable to non-enthusiasts, and keep prices stable until sales improve.

An example is the new Speedmaster Panda model. Despite its multi-layered lacquered dial, rhodium-plated subdial rings, applied indices, and ceramic bezel, it's hard to explain to the average buyer why this model is more expensive than a regular Speedmaster, given that the rest of the watch has remained largely unchanged.

Following the Money

Despite everything, Omega sold 460,000 units in 2025 - a significant volume. Even Blancpain with 18,500 and Breguet with 5,800 sold watches show impressive results, considering their niche status and high prices. The Swatch Group's strategy and other market players focused on the premium segment reflect an attempt to adapt to a K-shaped economy, where the very wealthy are less affected by economic crises, and affordable goods appeal to a broad audience. Although 2025 was not a breakthrough year, current strategies might be aimed at overcoming short-term difficulties for long-term benefits.

Rolex, Patek Philippe, Audemars Piguet, and Richard Mille demonstrate that targeting the ultra-wealthy is effective. Data from Vontobel and Deloitte confirms this trend. While entry-level and mid-level brands are losing sales, the luxury segment continues to grow. Rolex's Certified Pre-Owned (CPO) program also generates significant revenue. Other brands are expected to follow Rolex's example - for instance, Longines has already started offering limited vintage collections in its boutiques.

While this improves brand perception in terms of longevity and value retention, if enthusiast-loved brands continue to climb the price ladder, it could disappoint many and create a vacuum in brands, groups, and the watch market as a whole, making it unstable and potentially unsustainable.

TAG Heuer: Attempts to Rise Up

I cannot overlook TAG Heuer, which has previously attempted to rise into the premium segment with varying success. Following a strategic shift, the brand is once again focusing on split-second chronographs, tourbillons, and unique models. With in-house movements, technological innovations, and models appealing to both enthusiasts and the mass market, TAG Heuer, in my view, can successfully strengthen its position and increase its average sales price.

A Ray of Hope for the Ordinary Buyer

If the results of major brands generally confirm opinions in enthusiast communities, there is one more important point backed by solid data. I and many others have noted that microbrands and small independent manufacturers are filling the niche left by big brands, offering watches with features important to true connoisseurs at fairer prices. According to Morgan Stanley, brand Christopher Ward entered the top 50 for the first time in 2025.

Once a tiny internet startup with ambitions, Christopher Ward has grown into a brand with boutiques in key markets, unique and complex models approaching haute horlogerie, and a dedicated audience. In 2025, the brand sold 39,141 watches at an average price of 1,311 CHF, surpassing Oris in sales volume. More small brands are opening boutiques and collaborating with physical retailers, confirming the demand for independent brands. If there is any ray of hope in the current grim trends of the watch world, this is it.

Final Thoughts

Perhaps the most interesting indicator is the total number of watches sold and the gross turnover of the top 50 brands according to Morgan Stanley. In 2024, 13,366,560 watches were sold with a turnover of 35.258 billion CHF. In 2025 - 12,286,286 watches and 35.711 billion CHF. Despite a decrease in sales by more than a million units, turnover rose by 453 million CHF. Although this is largely due to price increases, the analysis of Tudor and Longines data shows that some brands successfully attract new buyers and convince them to spend more, while others lose buyers, only slightly increasing the average unit price.

I see this more as a redistribution of consumers rather than a significant growth of new buyers. Many newcomers who entered the watch world during the pandemic and continue to join are likely moving up the price scale and preferring well-known brands. These buyers are more likely to transition from Audemars Piguet to MB&F or Romain Gauthier than to expensive Omega models.

While I appreciate the presence of complex striking chronographs and understand that it's difficult for large brands to quickly change course, in the short term, they should focus on retaining customers and building positive relationships with the broad audience, rather than releasing complex and expensive models.

And Finally - Swatch Group

Initially, I planned to end the article here, but during editing, Swatch Group published an open letter criticizing Morgan Stanley's report. According to them, the report uses data that is not entirely reliable and cannot provide the accurate figures presented in the document. Publishing estimated data as definitive, according to Swatch Group, distorts information and can negatively impact the business of companies included in the report.

The conglomerate points out numerous inaccuracies: the average deviation in financial turnover is 24%, and in sales volume - 35%. Examples: Certina with an actual turnover deviation of -53%, Rado - +46%. Swatch Group believes that for greater objectivity, Morgan Stanley should publish a range of estimates rather than fixed figures.

I criticized some practices of Swatch Group not out of dislike, but on the contrary - because there are brands within the group that truly inspire me. The Morgan Stanley report has become a point of discussion for the economic success of brands, and Omega's decline can negatively impact investors. Enthusiasts use this data to argue against certain products and practices. If the data is incorrect, these conclusions become even less substantiated.

Swatch Group publishes an annual report for the group as a whole. Despite lower sales compared to the previous year, net profit was 25 million CHF - significantly less than 219 million CHF in 2024, but still a profit in a soft market. The watch market is subject to fluctuations, and one year does not determine the fate of a long-lasting company.

In my opinion, the truth lies somewhere in the middle. Morgan Stanley has likely conducted enough research to publish accurate data but could have presented the information with a clearer disclaimer regarding the reliability of sources. Swatch Group's publication of its data with discrepancies in both directions increases their credibility. Many Swatch Group brands, which have recorded declining sales in Morgan Stanley's report, may not have achieved desired results, but this does not mean they are in a bad position in the market.

This expert review reveals key trends and dynamics of the Swiss watch market in 2025, based on Morgan Stanley data and Swatch Group's response, providing a balanced perspective for industry specialists and enthusiasts.